“The capital is here. The talent is here. The question is whether allocators are paying attention.”

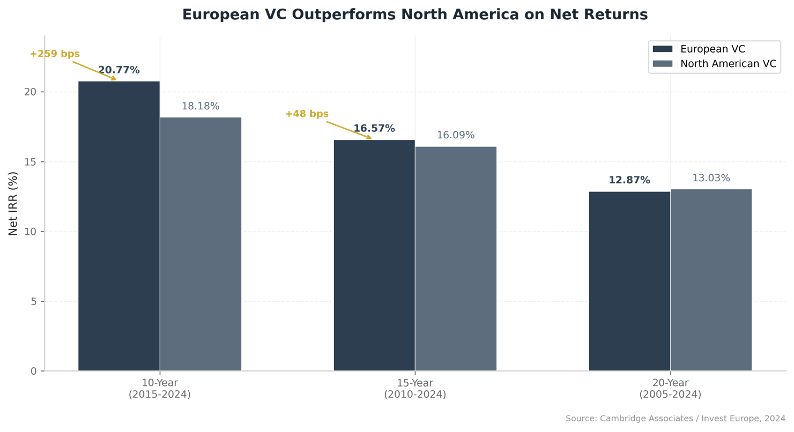

European venture capital has undergone a fundamental transformation that most limited partners have yet to recognize. European VC funds generated a net IRR of 20.77% over the ten years ending in 2024, outperforming North American peers at 18.18%. Over fifteen years, the margin holds: 16.57% versus 16.09%. These figures come from the Invest Europe / Cambridge Associates Performance Benchmark Report (June 2024), based on 223 European funds with €42.3 billion in total capitalization. Yet allocator narratives remain anchored to perceptions formed during Europe's fragmented past.

This is the quiet reordering: a structural maturation occurring beneath the threshold of mainstream investment consciousness, creating opportunity for those who recalibrate early and risk of misallocation for those who do not.

The Returns Refute the Old Story

The figures deserve scrutiny. The Cambridge Associates dataset encompasses 223 European VC funds with €42.3 billion in total capitalization, compared to 2,500 North American funds at €561.6 billion. The European sample is smaller, and it includes one outlier fund with an IRR exceeding 100% that lifts the average. But the directional signal is clear: Europe's ecosystem has developed the capability to generate world-class returns.

Vintage-level analysis reinforces this. The 2011 vintage achieved a TVPI of 7x and IRR of 37%; the 2016 vintage reached 3.7x TVPI and 33% IRR. The weak 2021–2022 vintages (TVPI ~1x) reflect global valuation cyclicality, not European dysfunction — identical patterns characterize US VC vintages from the same period. In the British Business Bank's 2025 UK Venture Capital Financial Returns report, surveyed GPs most often cited the 2025 vintage as the year they expect to generate the strongest returns.

€59 Billion in Dry Powder

European VC funds held approximately €59 billion in uncalled commitments at end-2024, up from €50 billion+ in 2023. Deal value reached €66.2 billion in 2025 (up 5.1% YoY), even as deal volume contracted 20.6% — a value-over-volume pattern indicating selectivity characteristic of mature markets.

Geographic dispersion is equally significant. Southern Europe achieved 6.3x fundraising growth over the decade; France and Benelux 3.7x; the Nordics 3.4x. This is capital responding to genuine entrepreneurial emergence across the continent, not recycling within established networks.

27,000 Startups and the Deep Tech Shift

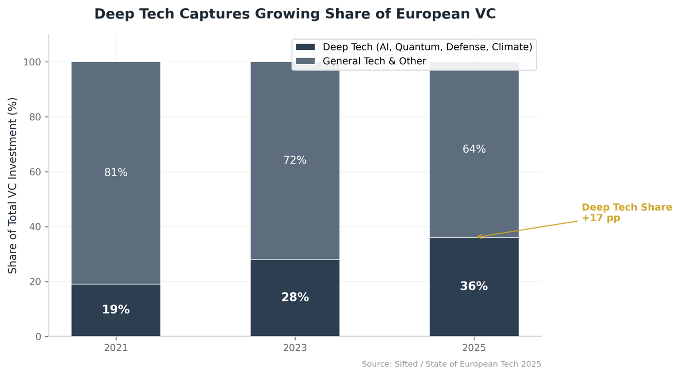

Startup formation accelerated dramatically in 2025: approximately 27,000 new technology ventures, a 60% increase from 2023, per Atomico's State of European Tech report. The composition has shifted decisively toward deep technology — AI, quantum computing, climate technology, and defense/dual-use applications.

Deep tech captured 36% of European VC dollars in 2025, up from 19% in 2021. AI alone commands 35.5% of deal value, with emphasis on efficient architectures, regulatory compliance integration, and “sovereignty” framing. Companies like Mistral AI (€1.7 billion Series C), Helsing (€600 million Series D), and DeepL (a $300 million funding round at a $2 billion valuation) demonstrate world-class capability with varying capital strategies. DeepL, which reached unicorn status with comparatively modest capital relative to frontier-model peers, illustrates the more measured scaling and operating discipline often found in European technology companies.

Why the Narrative Lags

If the data is so clear, why hasn't allocator behavior shifted? Three factors sustain the perception gap. First, historical fragmentation — 27 national regulatory regimes created genuine transaction costs that have diminished but persist in allocator mental models. Cross-border activity has rebounded strongly post-2015, yet the association with complexity remains.

Second, Europe's capital-constrained environment produces selection effects. European startups raise at median valuations roughly half those of US peers ($6.5M vs $14.6M, per Equidam 2025), not because they are inherently more capital efficient, but because smaller European fund sizes and higher underwriting thresholds set a higher bar to advance.

Third, allocator geography shapes capital flow in revealing ways. US allocators face familiar barriers — venture teams organized by stage rather than geography, and career risk favoring consensus allocations to established US managers. Japanese investors have demonstrated sustained appetite for European VC since the EU–Japan Economic Partnership Agreement came into force in 2019. Research by NordicNinja and Dealroom finds that Japanese-linked investors have participated in more than €33 billion of European startup financing rounds since 2019, around six times the volume recorded in the previous five years, and now feature in roughly 6% of all VC investment by value in Europe, with about 70% of 2024's flows directed toward deep tech and AI. Middle Eastern sovereign wealth funds, including Mubadala and ADIA, have also stepped up global deployment; MENA sovereign investors collectively deployed about $56.3 billion across 97 transactions in the first nine months of 2025, with roughly 28% of that capital going to Europe, including the UK.

The structural misalignment is starkest at the pension fund level: European pension funds allocated just 0.01% of AUM to VC in 2024, versus 0.03% for US pension funds. Equalizing that threefold gap would unlock an estimated $210 billion over the next decade. This is not a market seeking capital; it is capital seeking conviction.

The Entry Window

The convergence of €59 billion in dry powder with demonstrated founder quality improvement creates a distinctive deployment window for 2026–2028 commitments. Capital must be deployed within fund investment periods, creating sustained availability even if macroeconomic conditions deteriorate.

For allocators, the relevant question is not which ecosystem performed better over the past twenty years, but which is positioned for the next ten to fifteen. The progression from slight twenty-year underperformance to substantial ten-year outperformance traces a clear convergence trajectory. The capital is here. The talent is here. The returns are here. The only remaining variable is attention allocation — and that is a choice sophisticated investors make, not a condition markets impose.

The access question is where structure matters. European VC remains complex, which created the perception gap, and also creates the selection premium. Identifying which managers have the sourcing networks, operational discipline, and sector depth to compound over a full cycle is not a task that scales through direct allocations alone. A fund of funds operating with on-the-ground European presence — conducting systematic due diligence across emerging and established managers, building portfolio construction across vintages and verticals — converts ecosystem complexity into a structural advantage rather than a barrier.

Lumen is built for precisely this: a Luxembourg-domiciled fund of funds focused exclusively on European VC across technology and life sciences, with the regulatory infrastructure to engage institutional LPs across jurisdictions and the manager relationships to access funds that do not broadly market. The entry window is open. The access mechanism exists.